Hey, Retailer – Is a Unicorn Eating Your Lunch?

A new breed of retail business is emerging to take the place of those who failed to innovate for the new economy.

The failure of traditional retailers to evolve and adapt to the new economy has been well documented. Far less attention has been given to the key characteristics of the new breed of retailers stealing their market share. One way to identify the type of retailer who may dominate the future retail landscape is to look at the freshly crowned Unicorns of the last 12 months. Who are these new players whose businesses have surpassed USD $1 billion valuations? And what can traditional retailers learn from their defining traits?

Is a Unicorn Eating Your Lunch?

Err, what’s a unicorn?

Yes, a Unicorn is any start-up that reaches a USD$1 billion dollar market valuation, as determined by investment. The term, coined by Aileen Lee, founder of Cowboy Ventures, describes the statistical rarity of such businesses. Unicorns are certainly not the be-all and end-all. Camels, and their resilience through extended periods of adverse conditions, are emerging as desirable investment targets in the current COVID-19 business environment. But Unicorns continue to be strong indicators of where the world’s savviest investors see the greatest growth potential.

It’s important to understand the criteria influencing investors and driving these soaring valuations. Whilst they may differ from one sector to another, these are the top 8 criteria we see for Retail start-ups:

- User Adoption – Is the business solving a genuine customer or market problem? And is it evident through adoption?

- Traction – Is revenue growing rapidly and sustainably?

- Scalability – Is the operating model well-honed? And is it scalable to drive growth across geographies, channels or categories?

- Capability – Is the business led by an experienced team with the ability to keep innovating?

- Brand Awareness – Is the business buzz-worthy? Has it already begun to generate fame or notoriety in the press, on social media or through word-of-mouth (ideally with limited ad dollar spend)

- FOMO – How many other investors are circling or have already invested?

- Exit Scenarios – is there a clear potential pathway for triggering an exit event like an IPO or trade sale (ideally in a 3-5 year time frame)?

- Profitability – do the P&L metrics stack up? (Profitability is less of a concern in many other tech sectors. This is particularly true of early investment rounds where the focus is almost exclusively on top-line growth. But when it comes to retail and e-commerce start-ups, the bloody trail of failed e-commerce businesses – 90% fail within 120 days! – means that margins, cash flow and overall financial modelling will be far more heavily scrutinised).

In this list, we find the first key lesson for traditional retailers. All these criteria are worth considering as drivers of reinvigoration in traditional retail. The retailers who are struggling most are failing most obviously on three of the eight – User Adoption, Scalability and Capability. The questions they should be asking themselves are:

- Are we solving real and tangible customer problems with our products, channels and go-to-market model? If our offering has become outdated how do we evolve to stay relevant and compelling?

- Is our operating model scalable? Will it enable us to drive future growth or at the very least sustainable outcomes for our stakeholders over an extended horizon? If not, what needs to change?

- Have we invested enough in talent and capability? Do we have the right people on board and how do we continue to invest in their development to ensure they can drive continuous evolution?

And the best-dressed Unicorns are…

CrunchBase’s Unicorn Leaderboard estimates that there are currently 594 unicorns in the world, up from 452 one year ago. A growing number of them are e-commerce or marketplace platforms – in fact, they make up 16 of the new entries. They join the other retail ventures admitted to the Unicorn club over the last few years. These include well-known brands like Warby Parker, Gilt Group, All-Birds, FlipKart, FarFetch and LetGo.

Interestingly, e-commerce and marketplace platforms are amongst the fastest-growing category of unicorns. According to Fleximise.com, retail was the 4th fastest category. Retail Unicorns take on average 4 years to reach their billion-dollar valuation. This has them sitting behind Real Estate (2 years), OnDemand (3 years) and Social (4 years). But they sit well ahead of Unicorns hailing from FinTech (6 years), Healthcare (7 years), Cybersecurity (7 years) and Entertainment (9 years). Walmart-owned Jet.com holds the record as the fastest retail Unicorn (4 months). And online sports apparel retailer Fanatics slogged it out for 17 long years to make the cut.

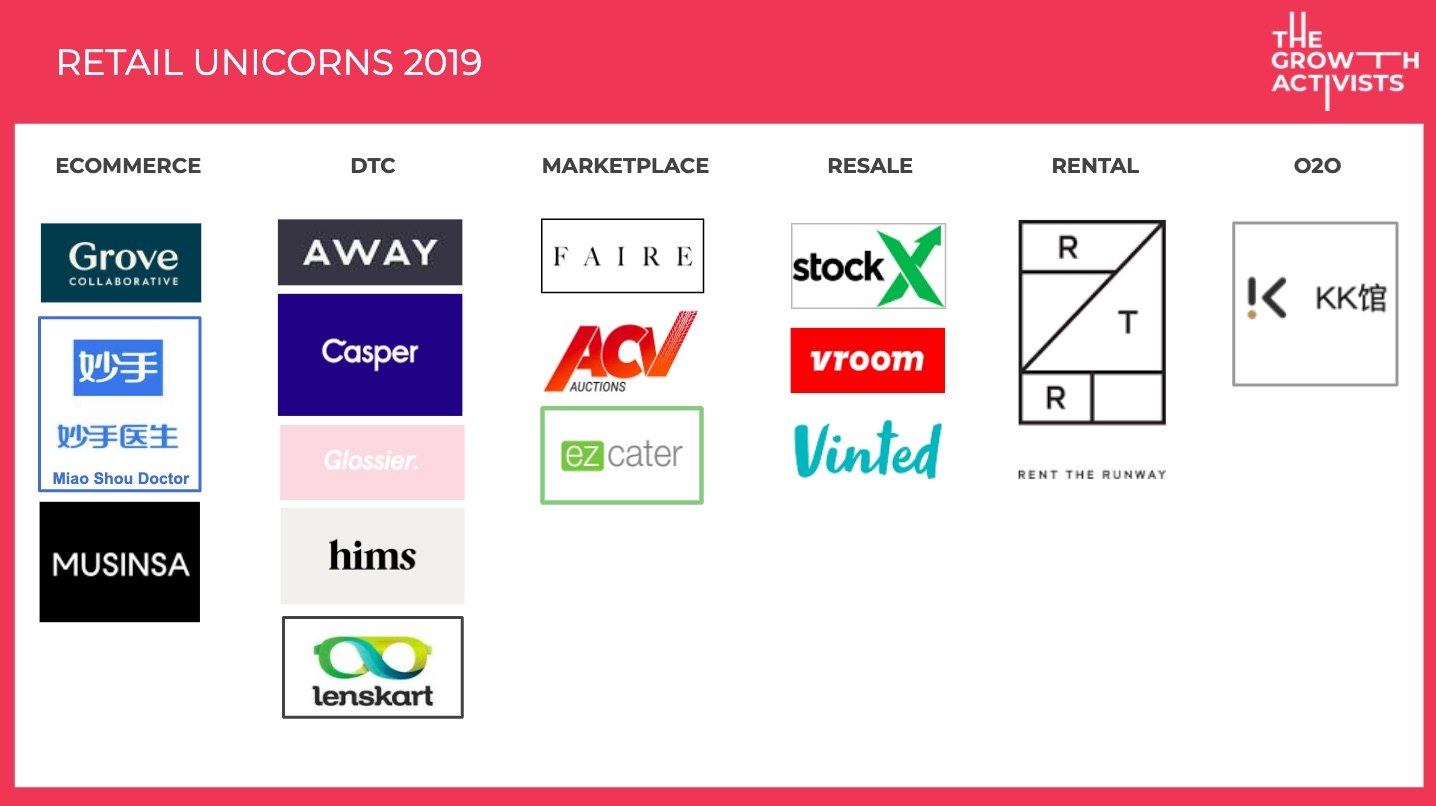

But what is most interesting about this year’s 16 new entries is the subcategories of retail they fall into. We’ve divided them into 6 key groups:

- E-commerce

- Direct-To-Consumer (DTC)

- Marketplace

- Resale

- Rental

- Online-to-Offline (O2O)

E-commerce

2019 saw three classic multi-brand e-commerce platforms reach billion-dollar valuations.

San Francisco-based Grove Collaborative is a purpose-led business with B Corp certification. It focuses on making it easy for customers to find natural and sustainable home essentials.

Musinsa is a Korean fashion commerce venture that combines four key elements – a fashion magazine, a fashion distribution platform, an online shopping mall, and online promotion services.

And Miaoshou Doctor is a Chinese pharmaceutical e-commerce business that has received funding from big-name investors including Sequoia Capital China and Tencent.

Defining Traits: Grove Collaborative and Miaoshou Doctor solve tangible customer problems in non-discretionary product categories (home cleaning and pharmaceuticals) whilst Musinsa is distinctive for the breadth of complementary content it brings together under a single umbrella.

Key Take-Out: As excess consumption continues to contract in a post-COVID19 economy, retailers must rebalance their offering of discretionary versus non-discretionary products, and show greater value around those categories which may be deemed unnecessary.

DTC

Direct-To-Consumer is the most crowded category. Four of the new entries are from the US and one is from India.

High-end luggage maker Away has generated major hype with customers (and the investor community). They’ve built their brand around stylish design and quality. They compete with traditional multichannel brands like Samsonite and Delsey. But at present, they face little DTC competition.

Mattress manufacturer Casper has instead had to work hard in a crowded market. Similar U.S. brands like Tuft & Needle and Leesa also offer ‘mattress in a box’ products with 100-day at home trial periods. Australian versions of this model include Koala, Ecosa and Sleeping Duck.

Glossier is a beauty brand founded by Instagram star and blogger Emily Weiss. The photogenic Weiss successfully transformed her followers into customers. The brand’s distinctive ‘millennial-pink’ branding and packaging have helped it establish a unique and aspirational identity.

Hims (and sister site Hers) call themselves a telemedicine company, selling men’s and women’s personal care products. Their brand is all about destigmatising conditions that customers shy away from discussing. In fact, their product range covers everything from erectile dysfunction to hair loss.

And finally, there is Indian start-up Lenskart which sells prescription eyeglasses, contact lenses and accessories online. Their meteoric rise has shown that the model pioneered by Warby Parker is applicable in other markets, albeit with some key differences. Most notably Lenskart’s broader pricing architecture starts with more affordable price points. Again, there are a number of local players who have also taken inspiration from the model. They include Sneaking Duck and Oscar Wylee.

Defining Traits: Away, Glossier and Hims are all built on distinctive and aspirational brand positioning. They also strongly leverage social media. They have built an enduring relationship with their customers through content. Casper and Lenskart, on the other hand, have had to be more aggressive with paid customer acquisition. This is due to the more crowded marketplace they compete in and the less distinctive nature of their brands.

Key Take-Out: The best DTC ventures prove that having a distinctive brand personality and image is a strong advantage. It enables the building of a customer base who will serve as advocates for continued growth. To compete with the best-loved DTC’s mono-brand retailers must focus on brand-building. They must also deliver a continuous content strategy that drives engagement.

Marketplace

The three ventures in this category all hail from the US.

Faire is an online wholesale marketplace that helps independent retailers find and buy interesting stock for their stores. One of its most popular features is the ability for retailers to discover brands that are not stocked on Amazon. This gives them a chance to be competitive and relevant to their customers. Many of the brands they stock are hand-crafted, eco-friendly or locally-made.

Another B2B marketplace is ezCater, which allows businesses to place online orders with caterers. They can order food for anything from a team meeting to a company conference. The platform uses ratings and reviews to ensure a quality experience. And finally, there is ACV Auctions. Its mobile platform helps used-car dealerships source their inventory through online auctions. Their model aims to save dealers time and effort in securing and transporting inventory. It also offers them peace of mind through features delivering trust and transparency.

Defining Traits: All three platforms solve customer problems by removing pain-points. They add tangible value to the process of sourcing products and services.

Key Take-Outs: Wholesale is not dead, it has evolved into online services that add value. The benefits are in making the discovery and purchase process faster, cheaper or more targeted. In a post-pandemic world, where business travel may never return to previous levels, online wholesale will be key. It may, to some extent, replace trade shows and showroom buying.

Resale

The Resale category is a hot one for investors. They see environmentally conscious millennials shifting away from disposable fast fashion and moving towards secondhand purchases of covetable products that will hold their value over time. This year saw three Resale ventures become unicorns.

The global market for sneaker Resale is worth a mind-blowing USD $6 billion annually, and Detroit’s StockX is now regarded as the leader in that space. It has surged ahead of sneaker sites like Grailed, GOAT and Sole Supremacy to make unicorn status. Close on its heels is Chinese sneaker resale site Poizon, which is also very close to a USD $1 billion valuations. Like luxury resale sites The Real Real and Vestiaire Collective, Stock X offers product authentication. This value-added service builds trust and credibility over generic marketplaces like eBay.

In 2019, Vinted became Lithuania’s first tech unicorn. The platform enables users to buy and sell second-hand clothes. It boasts over 25 million members across 11 European countries and makes money by taking a clip on the over €1.3 billion transacted on the site this year. Vroom is an American online used car marketplace that offers users an easier way to buy and sell. Its end-to-end platform covers logistics, reconditioning, car acquisition, front-end e-commerce and everything in between. Category extensions include financing and at home pick-up and delivery. Their aim is to provide a more satisfying customer experience.

Defining Traits: Stock X and Vinted tap into communities of passionate, product-obsessed customers. Stock X and Vroom are also distinctive for the value-added services included in the buying experience.

Key Take-Out: The time is now for Resale. COVID19 recessionary spending and growing environmental consciousness are dovetailing perfectly to change behaviours. Further opportunities exist for ventures to become ‘the eBay of….’. They must start by identifying the leading categories with sound resale value.

Rental

Rent the Runway appears to be the first rental platform to make the unicorn list. But based on evolving consumer behaviours around conscious consumption, it certainly won’t be the last. It started out as a site to rent a special occasion dress. It played on the notion that renting a ball gown for $200 was smarter (and kinder to the planet) than having a $1000 one hanging in your wardrobe. Particularly if that dress would only ever be worn once or twice. Rent The Runway has since expanded to also provide monthly subscription boxes of corporate and weekend clothes.

More recently it has also started to serve as a marketing channel to designers. Through rental, designers expose their brands to a new generation of potential future customers. Australian businesses who have adopted the model include GlamCorner and The Volte.

Defining Traits: This category addresses the customer’s need for guilt-free variety in their wardrobes. Rental delivers on savings, a smaller environmental footprint and access to usually unaffordable products.

Key Take-Out: With the number of key trends this model taps into, there is opportunity for it to extend to other consumer goods categories. This presents exciting potential to maverick retail entrepreneurs.

O2O

The final category is Online-to-Offline, also known as O2O, and the model hails from China. It refers to businesses that were born digital and expanded into bricks & mortar stores. This is different from e-commerce or DTC players with a guide or beacon stores. In their case, the store’s function is to support and supplement online sales. O2O entails a more significant investment in offline sales after the concept has been proven online. The model also leverages online data to drive offline success.

The one venture belonging to this Unicorn subcategory is KK Group, headquartered in Guangdong, China. It started as an e-commerce platform selling products from around the world, in categories like snacks, beauty and personal care. It gradually morphed into a marketplace for imported products with both online and offline channels. KK Group now operates 3 brands – KK Guan, KKV and The Colorist – with over 100 stores in 70 cities. The data-driven group regularly updates product assortments based on demand.

Defining Traits: What makes the O2O model most unique is that they remain digital-first in the running of their offline operations. They rely heavily on technology and data to drive success.

Key Take-Out: This model provides retailers a glimpse into the future of omni-channel retailing. We may see more ecommerce and marketplace ventures expand with intention to offline, particularly when they see opportunities to use their online edge to disrupt offline. They will look to leverage their data capability as an unbeatable competitive advantage over old-world retailers.

Unicorn School is out

The key lessons for retailers are many. First and foremost these ventures provide insights into where the entire retail category may be shifting. What is clear is that the best new ventures in the sector are doing the following:

- Solving tangible customer problems with their products

- Delivering value in terms of more effective, economical or time-efficient transactions

- Tapping into key macro-trends (like environmentalism or buying ‘small & local’) that will be impacting consumer behaviours,

- Investing in the creation of distinctive and aspirational brands

- Building and nurturing engaged audiences through compelling content

- Taking a digital-first approach to omnichannel retailing, leveraging online insights to offline

One further hugely significant lesson is that only one of the 16 ventures has a strong brick & mortar presence. Thud! Let that one sink in. Whilst VC-funding is heavily tech-biased, it is still an indicator of where investors see future value. And that is squarely in digital-first businesses with a distinctive edge.

COVID19 has certainly forced many traditional retailers into the future with new technologies. The ongoing need to keep shoppers and employees safe will require the introduction of even more technology. But retailers will need to go beyond technology as a hygiene factor. They must take a leaf from the Unicorn textbook to create new value in the customer experience. Their survival in the new world order will depend on it.

This article was first published on Inside Retail. The author, Rosanna Iacono, is Managing Partner at The Growth Activists. With over 25 years experience in retail and consumer goods, including global leadership roles with multinationals Nike and Levis, and C-Level roles in Australia, Rosanna leads The Growth Activists Retail & Consumer Goods practice. To discuss your retail growth strategy get in touch with Rosanna at rosanna@growthactivists.com